Loan Amortization Schedule: How to Calculate Accurate Payments

When you’re looking for a loan, it usually goes in three phases: researching and choosing a business loan, applying for the loan and getting approved, and then paying it off. As you’re just starting your loan shopping, chances are you stay mostly focused on the first two phases. You want to understand if you’ll qualify, what you’ll need to apply, and how long before you’ll get the cash. But, hopefully, you’re also asking yourself how you’ll pay it off. If you’re not prepared for the reality of making those regular loan payments, they can cause unending stress and even scar your financial future. Before you sign the dotted line on your loan, it’s critical that you understand exactly how the terms of your loan impact the pay-down process, so you know how much you’ll owe and when. Using a loan amortization schedule will help you do just that.

With a debt amortization schedule, you can compare payment schedules when you’re shopping for loans, break down your payments into an exact payment plan, and compare that payment schedule to your regular cash flow. This way, you can rest easy, feeling confident that you can afford your loan not just on paper, but in reality as the months and years pass by.

Let’s dive into what it is, how to understand it, how it evolves based on loan type, and a few of the best templates and examples out there.

What Is a Loan Amortization Schedule?

It is essentially an illustration of how you’ll pay down your loan over time. By showing each and every payment in the life of your loan in a standardized format, the debt amortization schedule helps you process the exact impact of your loan on your day-to-day cash flow and on your long-term bottom line.

Your Loan Amortization Glossary

If you’re looking at a loan amortization schedule templates or examples for the first time, you may come across a few terms you’ve never heard before, or that don’t match the terms on your loan agreement.

We’ll go into many of these terms (especially the different types of interest rates) later on, but to clarify any initial confusion, here are the terms you need to know:

Loan Amount: the total principal amount borrowed from a lending institution.

Total Repayment: the total amount to be repaid to the lending institution, including principal, interest, and fees.

Loan Period: the total time the loan will be outstanding, i.e. how long you’ll be paying off your loan.

Principal: this is the dollar value of the loan payment that is attributed to repaying the initial loan amount.

Interest: this is the dollar value of the loan payment attributed to repaying interest accrued on the loan.

Cumulative Interest: as seen on a standard loan amortization schedule, this is the dollar amount expression of interest paid for all periods of the loan.

Annual Interest Rate: the percentage of interest charged annually on a long-term loan, including origination or other fees.

Effective APR: actual percentage interest rate you’ll be paying annually when origination fees and other costs are factored in. Think of the effective APR as your “true cost” of financing.

Factor Rate: used only for short-term loans, the factor rate is a cents on a dollar figure expressing how much the lender will collect per dollar borrowed for the full term of loan. So with a factor rate of 1.2, if you borrow $10,000, you’ll repay $12,000.

Beginning Balance: the total amount owed on a loan before payment is made in a given period.

Ending Balance: the total remaining amount owed on a loan after payment is made in a given period

Now that we’re all speaking the same language, let’s take a deep dive into all things related to loan amortization. First, let’s discuss the three types of debt amortization schedules you’re most likely to encounter when taking on a business loan.

Types of Loan Amortization Schedules

Choosing the type of schedule to use for your loan will depend on how frequently interest on your loan compounds—daily, weekly, or monthly.

Most often, this compounding period will match the frequency that you make payments to the lender. If you’re making monthly payments, interest will compound monthly; interest on loans with daily payments compound daily; etc.

But there are exceptions to this rule, so make sure you clarify your loan’s compounding period—not just the payment period—when creating or reviewing your debt amortization schedule. This can make a big difference to your interest payments over time.

Monthly Loan Amortization

For a traditional multi-year medium term loans or SBA 7(a) loans with monthly payments, you’ll use a monthly loan amortization schedule to calculate your payments.

These loans will have a set, agreed upon monthly payment for the life of your loan.

Want to see a schedule of payments for your monthly amortizing loan? Check out a free downloadable monthly loan amortization schedule template.

Daily Loan Amortization

Loans that amortize daily are typically short term loans ranging from three-18 months. The lender’s profit from these loans are based on a factor rate, meaning you pay back a set rate of cents on the dollar for the amount borrowed.

With a daily amortizing loan, interest will compound daily Monday through Friday, excluding bank holidays, and you’ll typically make 20-22 payments per month (depending on the length of the month).

If you’re considering a short term loan with daily payments, use this free downloadable Excel template to create your own customized daily loan amortization schedule.

Weekly Loan Amortization

Before you jump to using a weekly loan amortization schedule, this is where it is important to pay attention to your loan’s frequency of compounding, as opposed to the frequency in which payments are due.

In many cases, loans with weekly payments actually compound interest daily, but offer a weekly payment option as a convenience to the borrower. There are also multi-year loans with weekly payments for which interest compounds weekly. For this type of loan, use this free downloadable weekly loan amortization schedule example.

Always check your loan agreement to make sure you’re using the right schedule for your loan’s interest compounding period.

All About Interest Rates

When it comes to figuring out a loan amortization schedule, interest rates are the most common spot where we see our customers get confused.

If you don’t truly understand the terminology and the way interest rates work, it’s easy to miscalculate the total cost of your loan, make mistakes in your debt amortization schedule, or make inaccurate assumptions when comparing loan products.

Let’s break down the reader’s digest version of everything you need to know about interest on your amortizing business loan.

Simple vs. Compound Interest

Though the percentage of interest paid on a loan can look congruent between loan products, the type of interest can make a big difference to the actual cost of your loan.

If your loan has a simple interest rate—which includes loans with factor rates—the interest is calculated only on the principal amount. For a $10,000 loan with a simple interest rate of 25%, your total cost (not including fees) is $12,500. Done.

But most loans have compound interest, meaning the interest is calculated both on the principal loan amount and on the accumulated interest. The rate at which compound interest accrues depends on the compounding frequency—daily, weekly, or monthly—which typically matches the payment frequency, so the more payments you make, the more compound interest you’ll accrue.

Types of Interest Rates

The way that interest rates are expressed can vary among lenders and among loan products. While it can be tempting to compare percentage interest rates from different loan products equally, doing so can leave out a number of factors and paint an entirely inaccurate picture of your true cost of borrowing.

Read on to make sure that you understand the interest rate for your individual loan product, and that you are plugging the correct numbers into your loan amortization schedule template.

Annual Interest Rate

Customarily, if you have a multi-year term loan with monthly payments, interest will be expressed as an annual interest rate. While this is close to an accurate estimation of the actual annual cost of your loan, it does not include the cost of origination and other fees. (See Effective APR below for more.)

Factor Rates

Used specifically for short-term loans with daily or weekly payments, a factor rate is the cost of borrowing expressed as a decimal figure. Factor rates typically range between 1.1 to 1.5, depending on your industry, how long you have been in business, your credit history, and your average monthly sales.

Calculate the total amount owed on your short term loan by multiplying the factor rate by the amount borrowed. For example, if you borrow $10,000 at a factor rate of 1.25 for a 6 month term, the total amount you’ll need to repay is $12,500 ($10,000 x 1.25 = $12,500).

One of the most common misconceptions we see from borrowers is the assumption that a factor rate of 1.25 is equivalent to a 25% interest rate. This is not correct. Because of the term of the loan, and because the cost is charged to the principal when the loan is originated, factor rates can’t be compared as equivalent to interest rates in this way. To compare apples to apples, you’ll need to calculate the loan’s Effective APR.

Effective APR

This here is the most important interest-related concept you need in order to make sure you’re making equal comparisons when shopping for loans. The annual percentage rate (APR) of a loan takes into account the loan’s principal amount, term (or length in months or years), interest rate, and any fees, including origination fees.

In the traditional lending sphere, banks and credit card companies are required to disclose the APR for any loan or line of credit—but alternative lenders aren’t required to play by those rules. That means the way your loan’s interest rate is expressed (through any of the interest rate types above) can leave out a lot of factors that may lead to your owing more than you expected.

To make sure you’re comparing apples to apples and plugging in accurate figures to your loan amortization schedule template, try using an APR calculator.

Reduced Interest Payments Over Time

When you review your loan amortization schedule, you might notice that in your first several payments, a larger portion of your payment is going toward the interest on your loan. As you scan down your schedule, you’ll see that over time, the amount of your payment going toward interest reduces, as more and more of your payment starts to be applied toward the principal value of your loan.

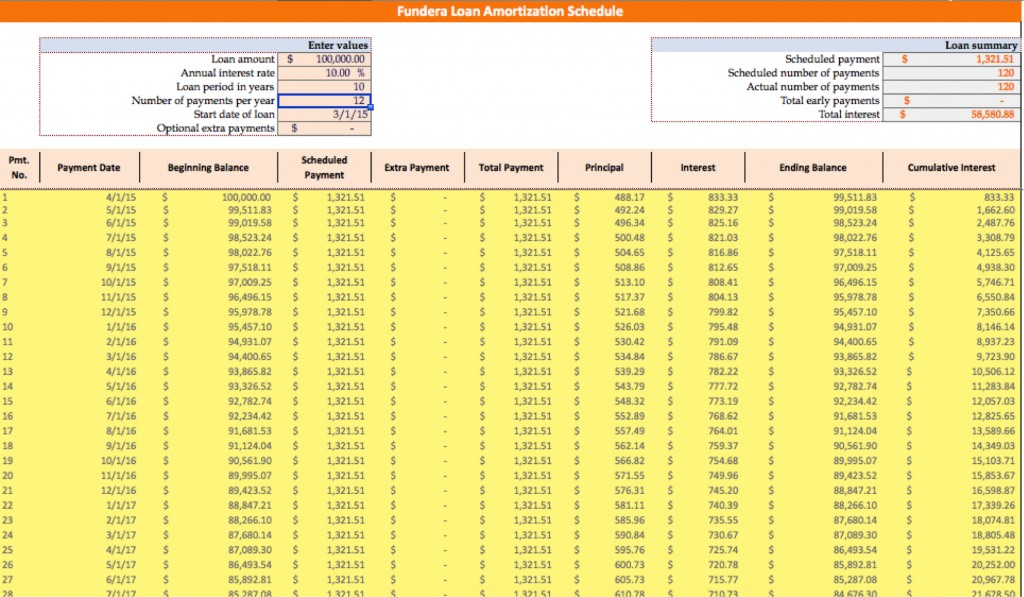

For example, let’s imagine we have a 10-year, $100,000 term loan with a 10% annual interest rate.

If you input those numbers into a monthly schedule template, you’ll see something like this:

Look at the very first payment of this schedule. You’ll see that out of the total monthly payment of $1,321.51, nearly two-thirds of that first payment ($833.33 to be exact) is going toward interest on the loan, with only $488.17 going toward paying down the actual principal that you borrowed. (So much for our simple math…)

By contrast, if we scroll down to the last several payments on this schedule calculator…

You see that for the very last monthly payment, almost all of the payment ($1299.66) goes toward principal, with a mere $10.92 being applied towards that last bit of interest.

So, why does this happen? It comes down to the fact that the beginning balance from the first payment ($100,000) is much higher than the beginning balance on the last payment ($1,310.59). So when you apply the compounded interest rate to that first number, you come out with a much higher interest payment than for the balance of the last payment.

Understanding Extra Payments

In the best-case scenario, taking on a business loan will have launched you on a path to off-the-charts revenue growth and profit potential. It’s practically raining money in your world. Right? Or at least you’ll have a little extra cash on hand.

If over the course of your loan your business has additional cash available on hand, either in a lump sum or at regular intervals, you might choose to make extra payments on your loan. Making extra payments can both reduce the length of your loan and save you money in compounding interest.

Let’s look at three different ways that borrowers typically choose to make extra payments, and calculate the time and money saved through extra payments in each scenario.[1]

1. Regular Extra Payments

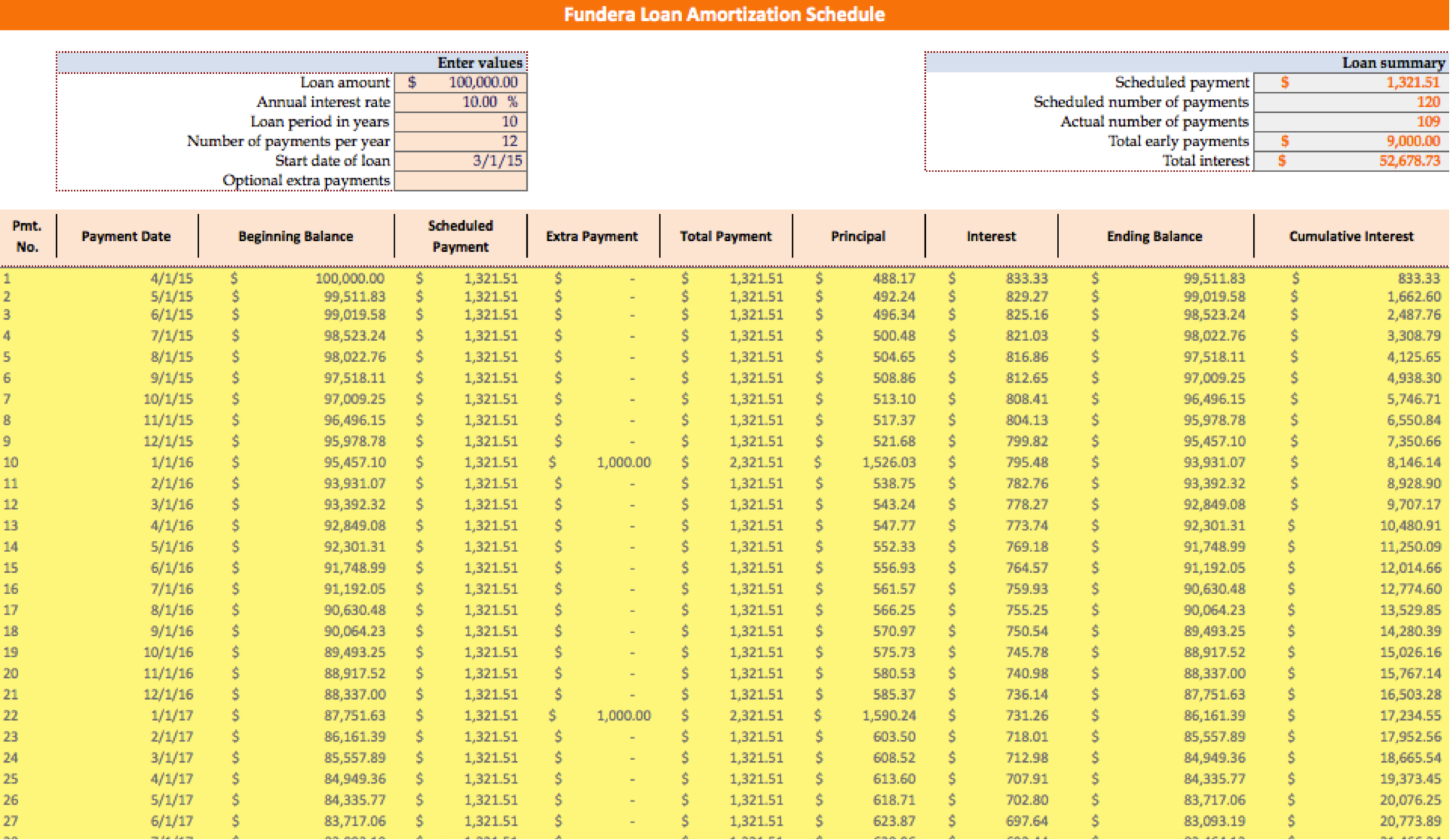

These are consistent extra payments over and above the agreed upon monthly payment amount. Using our earlier example, if your agreed monthly payment is $1,321.51, you might choose to pay $1500 per month instead, a difference of $178.49.

On your monthly loan amortization schedule example, you would input that difference into the “optional extra payments” box to view the impact of that extra payment:

As you’ll see, this regular extra payment will reduce your loan period by almost two years, and reduce the total interest paid on your loan from $58,580.88 to $46,576.20 (a savings of just over $12,000).

2. Sporadic Extra Payments

If you have a seasonal business or otherwise inconsistent revenue, there may be occasional times where you can afford to make extra payments on your loan. Let’s pretend, for example, that our $100,000 loan is for a fictional Christmas Tree business. Because of the influx of revenue every December, we can afford to make an extra payment of $1,000 every January. To calculate the effects of sporadic payments, you’ll have to input them manually into your amortization schedule formula:

By the end of our loan, we’ll have made total early payments of $9000, reduced our loan period by almost a year, saving over $5900 in interest.

3. Lump Sum End Payment

Finally, some business owners, as they near the end of the loan period, find that they just want it over and done with. If your business has become very successful and you have the cash on hand available, you may choose to make one lump sum payment to finish out your loan early. Or maybe you’ve chosen to sell your business, and you’re using part of those proceeds to pay off the rest of your loan.

Back to our $100,000 term loan, let’s look at the impact of paying off the last $20,000 in one lump sum:

By making a lump sum extra payment of $19,718.42 (the amount that was the ending balance of payment number 104 before we added in the extra payment), we reduced the loan period by one year and four months and saved almost $1500 in interest.

Of course, the value of making any type of extra payments depends entirely on their amount and frequency. Throwing in an extra $100 here or there isn’t likely to make a big difference. But every extra dollar you can put towards paying down your debt will make some impact toward shortening your loan period and saving you money.

If you’re considering making extra payments in any form, you can always go back to the loan amortization schedule to calculate the impact of that choice on the total length and cost of your loan.

Prepayment Penalties

Be aware that in some loan agreements there might be penalties for early payments. In these cases, unless you’re making a very large early payment, the prepayment penalty will likely be more than you would save by paying early. There are even some lenders who won’t forgive any interest if you pay off early. So, be sure to double check your loan agreement for any penalty clauses before you decide to make extra payments.

When Not to Use a Loan Amortization Schedule

While the debt amortization schedule is a very useful tool for many loans, there are some loan products that don’t amortize in a standard way—meaning the interest doesn’t compound on a regular schedule, and borrowers don’t make equal payments on a set schedule. Here are the three main instances where you likely won’t want to use one.

Merchant Cash Advance

When you take on a merchant cash advance, you’re agreeing to repay the lender for the principal plus interest and fees through a daily percentage of your business’s credit card sales. This can be a great solution for businesses with irregular revenue, because you’re not tied to a set daily or monthly payment that you may not be able to afford.

However, because your payments vary based on your day-to-day sales, this loan product does not amortize at a set pace, so the payments can’t be tracked through a standard loan amortization schedule calculator.

Invoice Factoring and Invoice Financing

Unlike most loan products, the cost of invoice financing and accounts receivable factoring are calculated based on a set factor fee, rather than an interest rate. Invoice financing is typically charged at a fee of around 0.5%-1% of the advanced amount per week. With invoice factoring, the typical fee is 1% per month.

In either case, the principal does not amortize, and there are no set payments to be made. Rather, the lender’s fee is deducted from the amount issued to the borrower.

Without amortization, compounding interest, or set payments, there’s no need to use a schedule calculator in this case.

Line of Credit

As opposed to a set loan with a set payment plan, taking on a line of credit works more like a credit card. You may have a balance on the line of credit, and your only requirement month to month is to make the interest payments on the principal. At any point, you may choose to pay back the principal on the line of credit at any pace you wish. While the interest compounds throughout the life of the line of credit, the debt would only start amortizing once you start paying down the principal.

Some business owners will choose to pay down the principal on their line of credit with regular payments on a set schedule, in which case you could in theory use a loan amortization schedule template to track that payment process. But in most cases, you’ll need to manually calculate your interest costs based on how you actually use and pay down the line of credit.

Know Before You Owe

No matter what type of debt you take on, it is imperative you fully understand the terms, conditions, and impact of your financing decisions, so that you can make the best and most informed decision possible for your business and your life.

We hope this information and the loan amortization schedule templates will help you feel informed and empowered to approach your borrowing choices with confidence.

Article Sources:

- Calcxml.com. “Extra Payment Calculator“

Meredith Wood

Meredith Wood is the founding editor of the Fundera Ledger and a GM at NerdWallet.

Meredith launched the Fundera Ledger in 2014. She has specialized in financial advice for small business owners for almost a decade. Meredith is frequently sought out for her expertise in small business lending and financial management.