Amortization Table vs. Payment Schedule: What’s the Difference?

Amortization Table: Definition

An amortization table is a data table that details the process of paying off a business loan. Specifically, the amortization table shows how much you are paying toward the principal and how much you are paying toward interest in each scheduled payment. The amortization table is essentially a visualization of the amortization schedule. An amortization schedule is a specific type of payment schedule.

When you begin repaying your business loan, part of your loan payment will be paid to the principal, and part will be paid to interest. As a reminder, the “principal” of the loan is what you borrowed, while the “interest” is, as you probably know, the cost of borrowing that money. If you have an amortizing loan, every payment you make isn’t equally split between principal and interest.

In fact, with amortizing loans, borrowers usually pay more of the interest upfront, leaving the principal for the end of a loan’s term. In other words, while you might be paying the same amount for that loan every week or month, what you’re paying toward will probably change. And understanding that balance impacts your prepayment options—but we’ll go over that in a bit.

First let’s learn a little bit about what amortization is, how an amortization table works, and how it all differs from a payment schedule.

What Is Amortization?

Amortization is the loss of value of intangible assets. When applied to loans, it means that the amount you pay in interest is compounded, and dependent on the amount of principal remaining on the balance. Early on, a majority of the money from your payments will go toward paying off the interest. With each subsequent payment, more will go toward paying back the principal.

Why does this happen? It comes down to the fact that the amount you owe when you make your first payment is greater than the amount you owe when you make subsequent payments. So when you apply the compounded interest rate to your initial balance, you come out with a much higher interest payment than for the balance of the last payment.

The difference between an amortizing and a non-amortizing loan is that the interest does not compound on a non-amortizing loan. In other words, the amount of interest you pay each payment period remains the same. The main benefit of an amortizing loan is that often it can be paid back early—thereby saving the borrower from paying additional interest on the loan. Non-amortizing loans cannot be prepaid (or have penalties for prepayment), to ensure that the lender receives full interest on the loan. Lenders offer amortizing loans because it allows them to receive a bulk of the interest on the loan early.

Generally speaking, if you have an amortizing loan, it makes financial sense to pay it back as quickly as possible, as this will ensure you pay the least amount of interest.

Amortization Table: How It Works

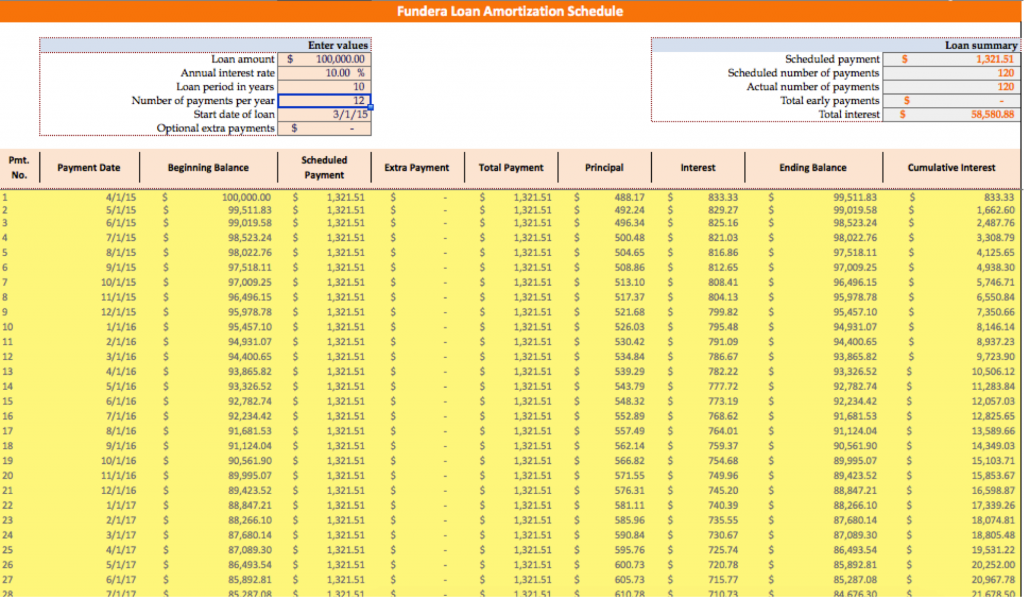

If you have an amortizing loan, you’ll be able to create an amortization table for your loan. An amortization table shows how much you are paying toward the principal and how much you are paying toward interest in each scheduled payment. To help you better understand how it works, let’s break down a loan amortization table column by column.

In the far left column you’ll see the payment number, starting at one, and ending with the last payment of your loan. So, if you have a two-year loan with monthly payment periods, you’ll see the numbers one through 24. This just shows how many payments you’ll make over the course of your financing. Note that loans can also amortize weekly or even daily.

The second column displays the date of that payment. Remember, paying on time and in full helps you build your business credit as well as avoid late charges. Beginning balance, in the third column, is pretty self-explanatory: that’s how much of the loan you have left to repay. The fourth column shows what you’ll be paying, and the next two columns indicate any extra payments and the full total, too. This generally remains the same.

The seventh and eighth columns are where things get interesting. As you can see, that scheduled payment gets broken down into principal and interest. As you go down the length of your payment, you can watch the principal portion increase while the interest amount decreases. That’s because your beginning balance drops with each payment, so naturally the interest on that amount is lower. But also notice how, as we mentioned earlier, you’re paying more interest in the beginning and more principal towards the end of your loan cycle.

Finally, the ninth column shows your balance after that row’s payment, while the tenth column tracks all the interest you’ve paid to-date.

What Is a Payment Schedule?

What amortizing and non-amortizing loans have in common is that they both come with a payment schedule. A payment schedule is simply a schedule of all the payments you have to make throughout the term of the loan. It shows the dates of each of your payments and the payment amount—the first four to six columns from the amortization schedule above, basically. However, it doesn’t break down how much of your payment goes towards interest or how much gets applied to your principal. It’s straightforward, but much less informative.

Amortization tables, on the other hand, actually give borrowers some useful and transparent information in terms of how much they are paying in interest. A payment schedule will show you the payment due and on what date, but it won’t reveal much more. They’re both useful, but for the savvy small business owner, an amortization schedule can give a lot more.

Amortization Table: Making Prepayments

Once you get your hands on your amortization table, look at the figure at the bottom of the interest column. In the example from earlier, the very last payment—#120—has only $10.92 in interest, while the first had $833.

Why is this important? Well, you might have the ability to pay a loan off early with a full prepayment, or at least make partial prepayments when your cash flow allows. But you’ll need to make sure you review your loan documents carefully to see how prepayments are applied. If they go directly towards the loan principal, they can reduce the amount of interest you’ll pay in the long run, especially if you make the prepayments early on in the loan. Prepayments made later on in a loan won’t save you as much money, because as you can see, most of your interest has already been paid to the lender.

Also, watch out for prepayment penalties—fees charged by the lender for the privilege of paying the loan down early. Most amortized business loans don’t have prepayment penalties. But if your loan does, these penalties completely wipe out the benefit of paying your loan off early.

Amortization Table: How to Get One

Some lenders only provide a payment schedule, so borrowers don’t know how much of their payment goes to principal and how much goes to interest. The solution? Just ask them for one. And be sure to read the fine print of your loan agreement carefully, because if you want to pay the loan off early, you may only get a “discount” on the interest you would have paid instead of avoiding paying the remaining interest altogether.

Also, some lenders who provide payment schedules can’t provide amortization tables. If these lenders allow prepayments, they’ll usually give you a discount on your remaining total, both principal and interest. We see this primarily with short-term lenders.

Amortization Table: How to Create Your Own

If you can’t get an amortization table from your lender, try calculating your own amortization table using one of the handy loan amortization table tools on our Know Before You Owe page. You’ll need to know your loan balance, total amortization time (the total time you’ll be making payments on the loan), the amount of each payment, and your APR. If you don’t know your APR, use one of our APR calculators to get that figure first.

Where to Get an Amortized Loan

A variety of different types of lenders offer amortized loans. If you’re in the market, here are your options:

SBA Loan

The SBA guarantees fully amortized loans from partner banks. When it comes to business loans, SBA loans typically have some of the most generous terms on the market. However, qualifying for an SBA loan is extremely difficult. Generally, candidates must have an annual revenue over $180,000, a credit score greater than 680, and have been in business at least four years. You must also provide a myriad of paperwork in your application, offer business assets as collateral, and sign a personal guarantee.

Lending Club

An alternative to the SBA is Lending Club. Lending Club is an online lender that provides fully amortized small business term loans with no prepayment penalty. Loan amounts range from $5,000 to $300,000 on one- to five-year terms with an interest rate ranging from 5.9% to 25.9%. To qualify for a Lending Club term loan you need an annual revenue of at least $50,000, a credit score of 620, and your business should have been in operation at least one year. Note that you will be charged an origination fee for an amortized loan with Lending Club.

Amortization Table: Helping You Make Smart Financial Decisions

If you have an amortizing loan, it is imperative you create an amortization table. Seeing what you owe each payment period in terms of interest and principal will help you take the best approach when it comes to repaying your loan. In general, the more you know about amortization tables and payment schedules, the better armed you’ll be to make the best financial decisions regarding your business borrowing.

Sarita Harbour

Sarita Harbour is a freelance writer and small business and entrepreneurship contributor at Fundera. She specializes in both business and personal finance. A former financial advisor, Sarita has over a decade of experience in banking. Her work appears online at sites such as Forbes, Investopedia, Yahoo!, Capital One Spark Business IQ, and Business News Daily.